Kerrie became a Realtor as a way to leverage her passion into helping you achieve your Montana dream. Call Kerrie today to begin your own amazing journey! Call Kerrie today at 406.270.2614.

![]()

Uncovering The Sun

By Dillon Tabish // April 2017 // Outdoors Flathead Beacon

They dodge tumbling boulders and surging avalanches. Hunkered inside high-powered heavy equipment, they navigate a narrow, often invisible path that ascends into the sky, twisting and turning up the mountainside along jagged cliffs and over a minefield of unstable surfaces. They sculpt walls of winter in the cradle of ancient glaciers, cutting through 30- to 50-foot drifts and chewing up 4,000 tons — 8 million pounds — of snow per hour, 100,000 cubic yards per spring.

These high-pressure operations are part of the Glacier National Park Road Crew’s age-old mission prepping the iconic Going-to-the-Sun Road for tourist season, a spring rite that plays a pivotal role in the park and surrounding region.

Starting April 1 and usually spanning 10 weeks each year, the 20-person crew braves this 50-mile highway, one of the most treacherous thoroughfares on the continent and the primary path into Glacier.

848 St. Andrews Drive Unit #1312, Columbia Falls, MT 59912

MLS #21701158 Offered at $218,000

Enjoy golf course living at Meadow Lake Resort with this fully furnished and move-in ready 2 bedroom / 2 bathroom ground level condo in scenic Northwest Montana. A putting green and swimming pool with spa are right out your back door. A lockout feature and private entrance on the second bedroom enables you to live in the main condo and rent out the second bedroom for additional income. Or purchase this condo as an investment property as nightly / weekly rentals are allowed. It’s a short 25 minute drive to Glacier National Park and 20 minutes to downhill skiing and summer activities at Whitefish Mountain Resort. Call Kerrie Cardon at 406.270.2614 for a showing.

For more photos and information, click here…

The Magic Place

EPISODE EIGHT: OPEN ROAD

The Great Northern Powder Guides take you into the deep back country to find untouched powder.

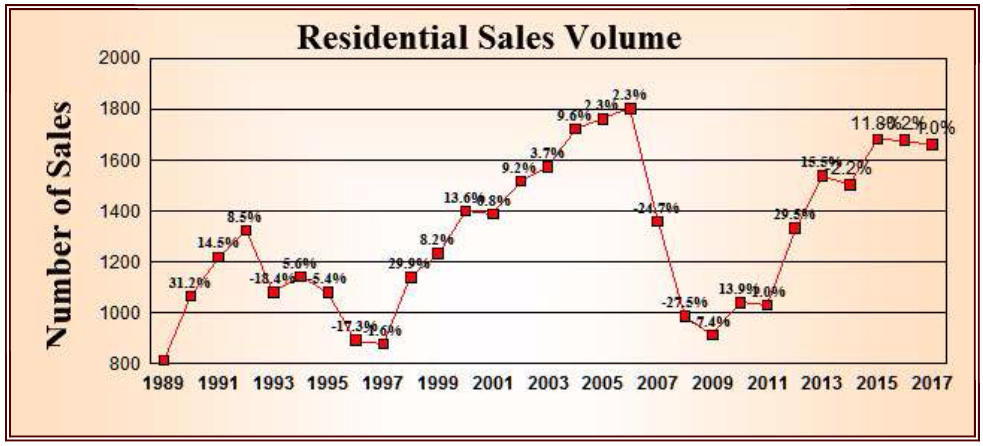

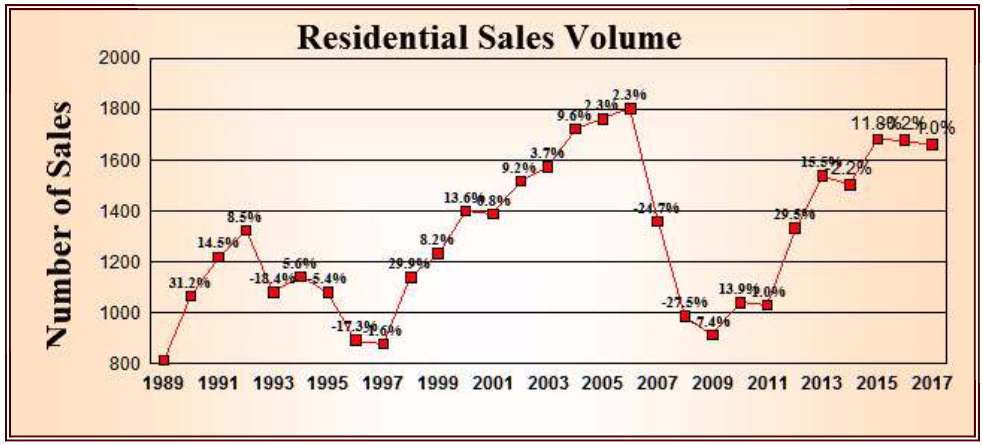

April real estate market trends update for Flathead County

By Jim Kelley, Kelley Appraisal, April 2017

Each month, Jim Kelley analyzes the trends in real estate sales in Flathead County of Montana. Click on the link to read to entire report.

Each month, Jim Kelley analyzes the trends in real estate sales in Flathead County of Montana. Click on the link to read to entire report.

April Real Estate Market Trends in Flathead County – click here to read the whole report.

Where are the plows?

See where the plows are today on Going to the Sun Road in Glacier National Park. Also see plowing photos posted by the crews. Click here to go to nps.gov.